There has been a firm

level of demolition activity in the first four months of 2015 and the two

largest owner regions, Asia/Pacific and Europe account for 88% of the tonnage

sold for recycling. Whilst the Indian Sub-Continent remains the main demolition

destination, recent activity has seen Bangladeshi breakers take the lead. This

month, we take a closer look at the country trends behind global demolition.

Busting The Bulk

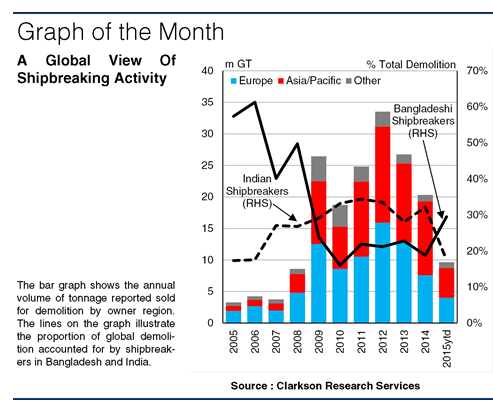

The world fleet has seen

elevated levels of ship recycling in recent years with an average of 27.2m GT

reported sold for demolition between 2009 and 2014.

Prior to this, the

shipping boom limited demolition activity and an average of 5.7m GT was

scrapped between 2005 and 2008. In 2015 so far, a reported 346 vessels of 10.8m

GT have been sold for recycling. On an annualised basis, this is an increase of

43% in terms of GT. This has been driven by a surge in bulker demolition,

particularly Capesize vessels, in response to historically low earnings and

fleet oversupply. Bulkers account for 74% of tonnage reported scrapped in the

ytd.

Who’s Driving

Demolition?

With the two largest

fleets, European and Asia/Pacific owners have accounted for 70-85% of

demolition volumes over the last decade. European owners have generally

recycled the largest volume of tonnage but more recently, Asia/Pacific owners

have matched European demolition volumes and last year they scrapped 4.1m GT

more than European owners (11.7m GT), accounting for over half of global

demolition (52%). In the ytd, Asia/Pacific owners are reported to have sold

4.8m GT for demolition compared to European owners’ 4.0m GT. This is largely a

result of Chinese demolition activity, boosted by the government’s domestic

scrap subsidy. Chinese owners demolished a record 6.7m GT last year, equivalent

to 30% of the global total, and they are reported to have sold 2.2m GT for

scrap in 2015 so far. Meanwhile, South Korean owners have scrapped 0.9m GT in

the ytd, equivalent to 5% of their start year fleet on an annualised basis.

Elsewhere, the Greeks are typically the most active European owners in the

demolition market and account for 54% of

the region’s ytd demolition (2.2m GT) compared to a 39% share last year.

German

demolition volumes have risen in recent years and alongside Norwegian owners,

they have scrapped a reported 0.4m GT each in the ytd – 20% of the region’s

total.

Bangladesh At The Front?

The majority of tonnage

is demolished in the Indian Sub-Continent and in the ytd Bangladeshi breakers

have scrapped a reported 3.2m GT, 30% of the global total. This compares to

1.9m GT reported demolished in India and is the first time that Bangladeshi

breakers have taken the lead since 2009. Firm bulker scrapping has boosted

Bangladeshi volumes, representing 88% of the country’s demolition in the ytd.

Further, recycling activity in India has been limited by currency volatility

and a weak steel market.

So, Asia/Pacific owners

have taken the lead in demolition but their European counterparts aren’t too

far behind. Strong Chinese demolition volumes largely explain this shift.

Meanwhile, Bangladeshi shipbreakers have scrapped the largest volume of tonnage

in the ytd.

Source: Hellenic shipping

news.

No comments:

Post a Comment